Home | No Surprise Act

No Surprise Act

YOUR RIGHTS AND PROTECTION AGAINST SURPRISE MEDICAL BILLS

When you get emergency care or get treated by an out-of-network provider

at an in-network hospital or ambulatory surgical center, you are protected from surprise billing or balance billing.

What is "Balancing Billing" (sometimes called "surprise billing")?

When you see a doctor or other health care provider, you may owe certain out-of-pocket costs, such as copayment, coinsurance, and/or a deductible. You may have other costs or have to pay the entire bill if you see a provider or visit a health care facility that isn’t in your health plan’s network.

“Out-of-network” describes providers and facilities that haven’t yet signed a contract with your health plan. Out-of-network providers may be permitted to bill you for the difference between what your plan agreed to pay and the full amount charged for a service. This is called “balance billing”. This amount is likely more than in-network costs for the same service and might not count toward your annual out-of-pocket limit.

“Surprise billing” is an unexpected balance bill. This can happen when you can’t control who is involved in your care—like when you have an emergency or when you schedule a visit at an in-network facility but are unexpectedly treated by an out-of-network provider.

You are protected from balance billing for:

Emergency Services

If you have an emergency medical condition and get emergency services from an out-of-network provider or facility, the most the provider or facility may bill you is your plan’s in-network cost-sharing amount (such as copayments and coinsurance). You can’t be balance billed for these emergency services. This includes services you may get after you’re in stable condition, unless you give written consent and give up your protections not to be balanced billed for these post-stabilization services.

Certain Services at an In-Network Hospital or Ambulatory Surgical Center

When you get services from an in-network hospital or ambulatory surgical center, certain providers there may be out-of-network. In these cases, the most those providers may bill you is your plan’s in-network cost-sharing amount. This applies to emergency medicine, anesthesia, pathology, radiology, laboratory, neonatology, assistant surgeon, hospitalist, or intensivist services. These providers can’t balance bill you and may not ask you to give up your protections not to be balance billed. If you get other services at these in-network facilities, out-of-network providers can’t balance bill you, unless you give written consent and give up your protections.

You’re never required to give up your protections from balance billing.

You also aren’t required to get care out-of-network. You can choose a provider or facility in your plan’s network.

When Balance Billing Isn't Allowed, You also have the Following Protections:

You are only responsible for paying your share of the cost (like the copayments, coinsurance, and deductibles that you would pay if the provider or facility was in-network). Your health plan will pay out-of-network providers and facilities directly.

Your health plan generally must:

- Cover emergency services without requiring you to get approval for services in advance (prior authorization).

- Cover emergency services by out-of-network providers.

- Base what you owe the provider or facility (cost-sharing) on what it would pay an in-network provider or facility and show that amount in your explanation of benefits.

- Count any amount you pay for emergency services or out-of-network services toward your deductible and out-of-pocket limit

State Balance-Billing Protections

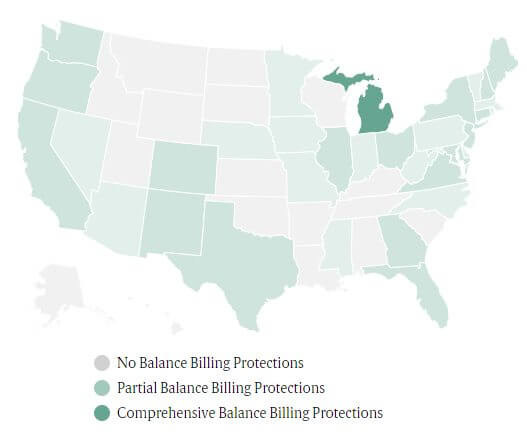

“Balance bills” primarily occur in two circumstances: 1) when an enrollee receives emergency care either at an out-of-network facility or from an out-of-network provider, or 2) when an enrollee receives elective nonemergency care at an in-network facility but is inadvertently treated by an out-of-network health care provider. Since the insurer does not have a contract with the out-of-network facility or provider, it may decide not to pay the entirety of the bill. In that case, the out-of-network facility or provider may then bill the enrollee for the balance of the bill. While 33 states have enacted laws to protect enrollees from balance billing, the scope of these protections varies as shown in the map below. Congress enacted the No Surprises Act in 2020 to protect most people who are not currently protected under this patchwork of state laws. This federal law goes into effect on January 1, 2022.

See here for the criteria used to determine which states have comprehensive or partial protections.

Michigan Comprehensive Balance Billing Protections

Protections Available

- State prohibits out-of-network providers from billing enrollees for any amount beyond in-network level of cost sharing

Above Protections apply to:

- HMO and PPO enrollees.

- For emergency services by out-of-network professionals and facilities; and non-emergency services provided by out-of-network professionals at in-network facilities.

Provided by all or most classes of out-of-network health care professionals.

Protections do not apply to:

- Ground ambulance services.

- Enrollees who consent to non-emergency out-of-network services.

- Enrollees in self-funded plans.